1 (800) 584-0324

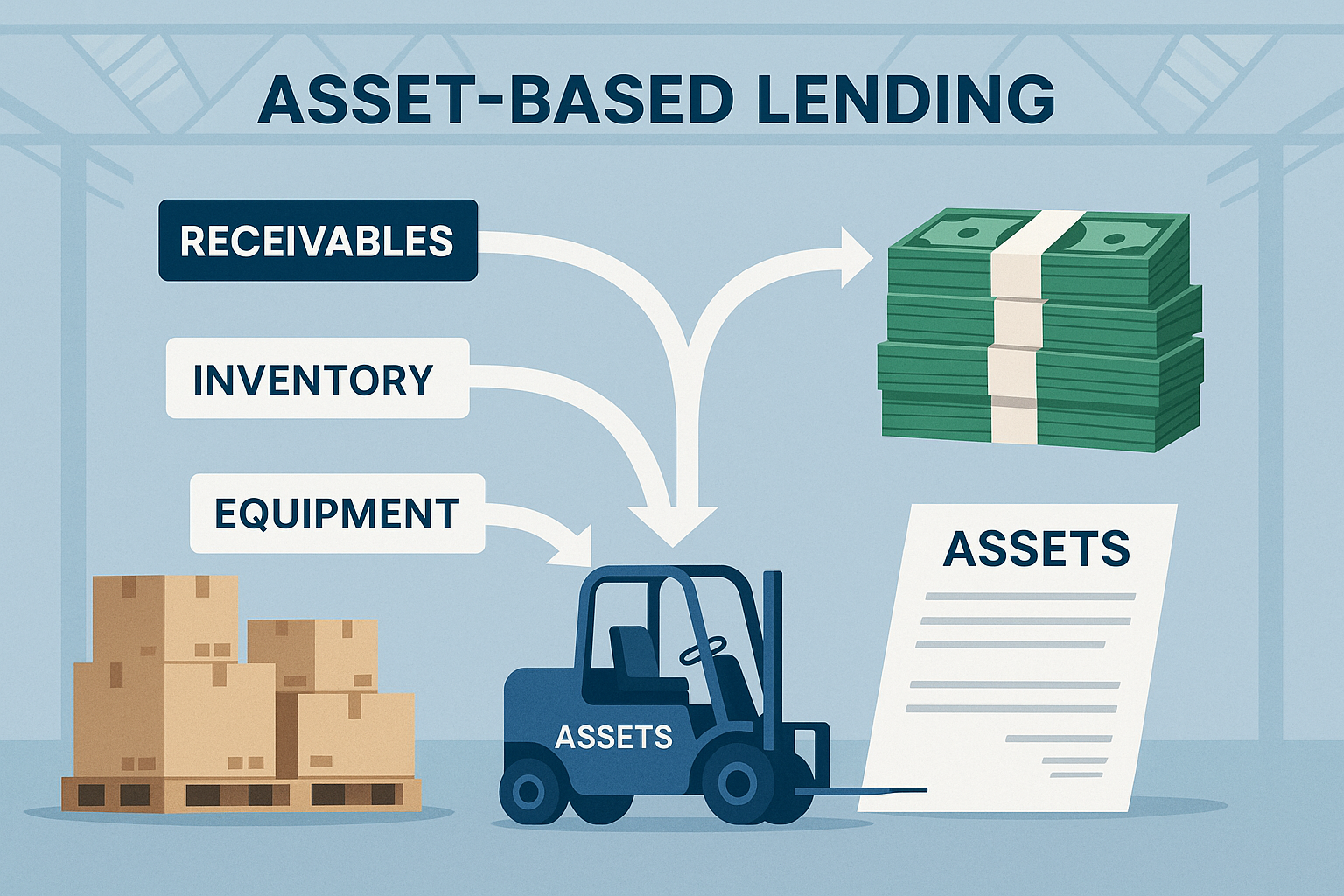

With banks tightening credit and interest rates fluctuating, many businesses struggle to qualify for unsecured loans. That’s where asset-based lending (ABL) comes in. By pledging receivables, inventory, or equipment, companies can unlock liquidity even if cash flow is uneven or credit history is limited.

In this guide, we’ll explain how asset-based lending works, the pros and cons, and when it’s the right financing option for your business.

What Is Asset-Based Lending?

Asset-based lending is a form of secured financing where loans or lines of credit are backed by collateral such as:

- Accounts receivable (A/R): Advance rates typically 70–90% of eligible invoices

- Inventory: Advances range from 30–70% depending on type and marketability

- Equipment or machinery: Collateralized at a percentage of appraised value

- Real estate (sometimes): Used in larger, hybrid ABL facilities

Unlike unsecured loans, approval depends more on the quality of assets than on past profitability.

Comment fonctionne le prêt garanti par des actifs

- Application & Collateral Review

The lender evaluates your receivables, inventory, or equipment. Clean, diversified A/R and marketable inventory improve advance rates. - Advance Rate & Borrowing Base

You receive a percentage of eligible collateral value. This creates a borrowing base, recalculated monthly or weekly. - Loan or Revolving Credit Facility

Funds are advanced as a lump sum (loan) or on-demand (line of credit). - Ongoing Monitoring

Lenders may require A/R aging reports, inventory updates, or field audits.

Pros of Asset-Based Lending

✅ Access capital when cash flow is tight

✅ Flexible revolving structure grows with sales

✅ Lower reliance on credit history compared to unsecured loans

✅ Can support turnarounds or high-growth situations

✅ Potentially larger facilities than unsecured alternatives

Cons of Asset-Based Lending

❌ Ongoing reporting & monitoring requirements (borrowing base certificates, audits)

❌ Advance rates below full asset value

❌ Higher fees than traditional bank loans (field exams, appraisal costs)

❌ Collateral encumbrance may limit other borrowing options

Asset-Based Lending vs. Unsecured Loans

| Factor | Prêt garanti par des actifs | Unsecured Loan |

| Approval Basis | Asset value & collateral quality | Credit score, financial history |

| Collateral Needed | Yes (A/R, inventory, equipment) | Non |

| Facility Size | Scales with asset base | Limited by creditworthiness |

| Reporting | Frequent monitoring & audits | Minimal ongoing reporting |

| Cost | Moderate (fees + interest) | Lower if strong credit, higher if weak |

When to Use Asset-Based Lending

- High-growth companies with strong sales but cash flow lags

- Seasonal businesses managing inventory cycles

- Turnaround situations where profitability is recovering but assets are solid

- Mid-market firms needing larger, scalable credit facilities

U.S. vs. Canada: ABL Options

- U.S.: Widely used in manufacturing, distribution, and retail. Private credit funds and banks both provide ABL lines, often $1M–$100M+. SBA loans are unsecured, so companies without collateral may qualify there instead.

Canada: Banks, BDC, and independent lenders offer ABL structures. The Canada Small Business Financing Program (CSBFP) focuses more on equipment and property loans but can complement ABL strategies.

Looking to unlock liquidity through asset-based lending? Agile Solutions structures ABL facilities across U.S. and Canadian lenders, helping businesses maximize advance rates and negotiate better terms.

👉 Book a consultation today at agilesolutions.global or email us at info@agilesolutions.global

#AssetBasedLending #WorkingCapital #InvoiceFinancing #BusinessLoans #SBALoan #BDC #CSBFP #PrivateDebt #CapitalMarkets