1 (800) 584-0324

When traditional banks say “no,” many entrepreneurs turn to fast, flexible financing products. One of the most popular is the merchant cash advance (MCA). But while MCAs promise quick access to cash, they come with trade-offs every business owner should understand.

In this article, we’ll break down merchant cash advance pros cons, explain how they work, and explore alternatives that may better support your long-term cash flow.

What Is a Merchant Cash Advance?

A merchant cash advance isn’t technically a loan. Instead, a provider advances a lump sum upfront, which is repaid by taking a fixed percentage of your future credit card or debit card sales.

- Advance amount: Typically $5,000–$500,000

- Repayment: Daily or weekly deductions directly from sales revenue

- Factor rate: Commonly 1.2–1.5 (e.g., borrow $100,000, repay $120,000–$150,000)

- Speed: Funds can arrive in 1–3 business days

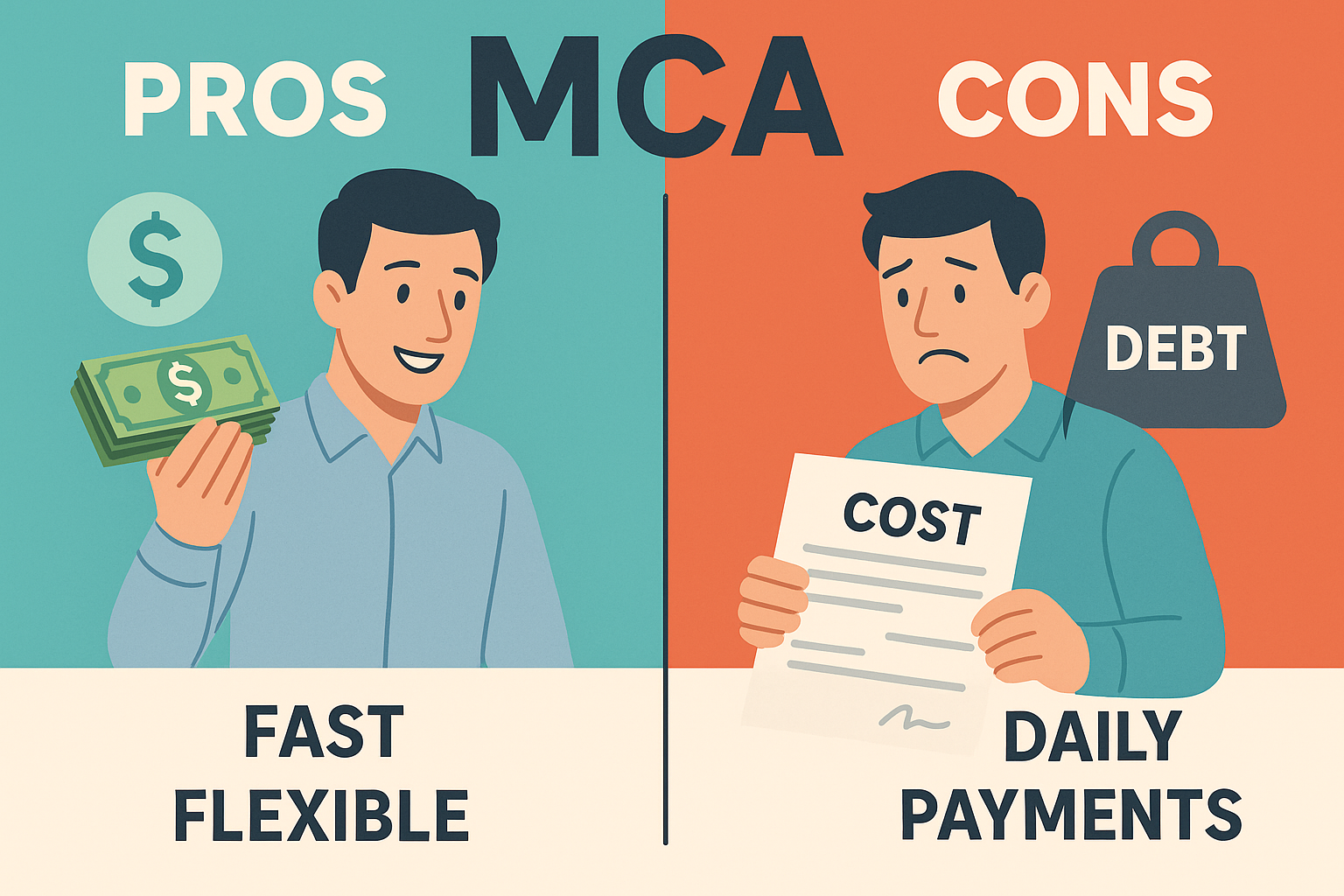

Merchant Cash Advance Pros

✅ Fast funding: Approval within days, no lengthy underwriting.

✅ No collateral required: Based on sales, not assets.

✅ Flexible repayment tied to sales: Lower payments when revenue dips.

✅ Accessible for weaker credit: MCA providers focus on cash flow, not just FICO.

Merchant Cash Advance Cons

❌ High effective costs: Annualized interest can exceed 40–80%.

❌ Daily/weekly deductions: Can strain cash flow during slow periods.

❌ No equity building: Unlike a loan secured by assets, MCAs don’t build ownership value.

❌ Potential cycle of dependency: Businesses may refinance repeatedly, compounding costs.

When a Merchant Cash Advance Might Make Sense

- Emergency repairs or payroll shortfalls

- Seasonal businesses bridging short gaps

- Firms unable to qualify for traditional credit but with strong daily sales

MCAs should be viewed as last-resort financing—best used short-term and repaid quickly.

Safer Alternatives to MCAs

If you’re weighing merchant cash advance pros cons, also explore these options:

1) Short-Term Business Loans

Structured repayment, often lower cost than MCAs, with terms of 6–24 months.

2) Business Lines of Credit

Draw only what you need, repay, and redraw. More flexible than MCAs, and interest applies only to amounts borrowed.

3) Invoice Factoring & Receivables Financing

Turn unpaid invoices into immediate cash without resorting to expensive MCA structures.

4) Equipment Financing

Secure funding against specific equipment purchases—often with competitive rates and longer terms.

5) SBA Loans (U.S.) or CSBFP (Canada)

Government-backed programs offering lower-cost financing for eligible businesses.

U.S. vs. Canada Context

- U.S.: MCAs are widely used by retail, restaurant, and service firms. Alternatives include SBA CAPLines and fintech-driven credit products.

- Canada: MCAs exist but are less common; businesses often use working capital loans or factoring instead.

Key Takeaway

The merchant cash advance pros cons balance comes down to speed vs. cost:

- Pros: Fast, easy, accessible

- Cons: Extremely expensive, risky for long-term cash flow

Before signing, calculate the true effective APR and compare against safer alternatives.

Considering a merchant cash advance but worried about costs? Agile Solutions helps businesses in the U.S. and Canada find affordable financing alternatives, from short-term loans to structured credit facilities.

👉 Book a consultation today at agilesolutions.global or email us at info@agilesolutions.global

#MerchantCashAdvance #BusinessFinancing #WorkingCapital #AlternativeLending #PrivateDebt #FinTech #SBALoan #CSBFP #InvoiceFactoring