1 (800) 584-0324

Cash flow gaps can stall growth even in profitable businesses. When customers take 30–90 days to pay invoices, you may need outside funding to bridge the gap. The two most common options are invoice factoring vs loan.

This article compares both financing tools—explaining how they work, their pros and cons, and how to choose the right one for your business in 2025.

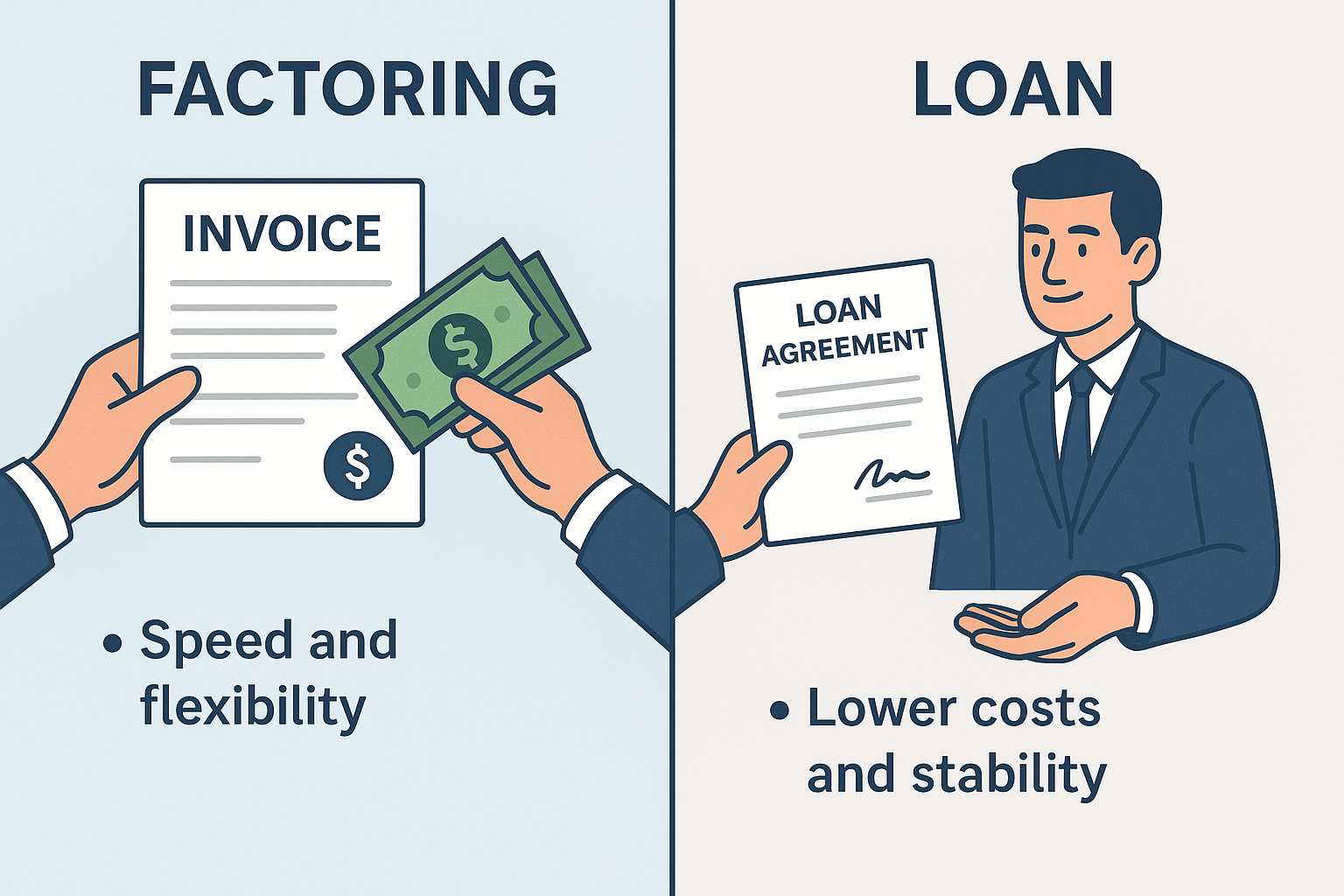

Invoice Factoring vs Loan: The Basics

Invoice Factoring

You sell unpaid invoices to a factoring company at a discount for immediate cash.

- Advance: 70–90% of invoice value upfront

- Remaining balance (minus fees) released when customer pays

- Repayment tied directly to customer receivables

Business Loan (or Line of Credit)

You borrow money from a bank, credit union, or alternative lender and repay over time with interest.

- Loan size: Based on financials, creditworthiness, and collateral

- Repayment: Fixed installments or revolving draws (for lines of credit)

- Independent of customer payment cycles

Pros and Cons of Invoice Factoring

Pros

✅ Immediate access to cash

✅ Approval based on customer credit, not yours

✅ Scales with sales (more invoices = more cash available)

✅ No new debt added to your balance sheet

Cons

❌ Higher effective cost than traditional loans

❌ Customers know their invoices are factored (may affect perception)

❌ Reliant on customer payment timelines

❌ Less control if factoring company manages collections

Pros and Cons of Business Loans

Pros

✅ Lower interest rates (especially SBA, BDC, or CSBFP-backed loans)

✅ Full control over customer relationships

✅ Predictable repayment schedules

✅ Builds business credit profile

Cons

❌ Longer approval process (weeks vs days)

❌ Requires strong financials, credit, and often collateral

❌ Adds debt to the balance sheet

❌ Fixed repayment even if customer payments are late

Key Differences: Invoice Factoring vs Loan

| Factor | Invoice Factoring | Loan / Line of Credit |

| Speed | Fast (1–5 days) | Slower (2–8 weeks) |

| Qualification | Customer creditworthiness | Your credit & financial strength |

| Balance Sheet Impact | Off-balance-sheet financing | Adds debt/liability |

| Flexibility | Tied to invoices (scales with sales) | Lump sum or revolving limit |

| Cost | Higher fees (1–5% per invoice) | Lower rates (prime + spread) |

| Customer Involvement | Customers may interact with factor | Customer relationships remain direct |

When to Choose Invoice Factoring

- You need fast cash tied to specific invoices

- Your business has limited credit history but strong customers

- Growth is outpacing cash flow

- You want funding that scales with sales volume

When to Choose a Loan or Credit Line

- You need a large lump sum for equipment, expansion, or refinancing

- You want lower financing costs

- You have strong credit and collateral

- You prefer to keep customer interactions under your control

U.S. vs. Canada Context

- U.S.: Factoring is widely used in industries like trucking, staffing, and manufacturing. SBA loans and bank credit lines remain lower-cost alternatives.

- Canada: Factoring is common in transportation and export sectors. Programs like BDC working capital loans and the CSBFP provide debt-based alternatives at lower costs.

How to Decide: Practical Checklist

Ask these before choosing invoice factoring vs loan:

- Do I need funds this week or can I wait 30–60 days?

- Is my customer base creditworthy enough for factoring?

- Do I want to avoid new debt on my balance sheet?

- Is cost or speed more important right now?

- How will this choice affect my customer relationships?

Not sure whether invoice factoring vs loan is the best fit? Agile Solutions helps businesses across the U.S. and Canada evaluate cash flow needs, structure lender-ready packages, and compare factoring vs credit lines across our multi-lender network.

👉 Book a consultation today at agilesolutions.global or email us at info@agilesolutions.global

#InvoiceFactoring #BusinessLoan #WorkingCapital #CashFlow #BusinessFinancing #SBALoan #BDC #CSBFP #PrivateDebt #CapitalMarkets